As you may know, Renta period for tax year 2025 is really near, starting the 8th of April and finishing 30th of June.

If you are a tax resident in Spain under the regular tax regime and you have earned work income from abroad; this post will help you understand the different options you have to declare it in your income tax return 2025.

1. As a tax resident in Spain you have to declare the worldwide income.

Article 2 of the LIRPF (Ley del Impuesto de la Renta de las Personas Físicas, the law that regulate the personal income tax law in Spain), states the following:

The scope of this tax is the taxpayer’s income, defined as the totality of their earnings, capital gains and losses, and any income allocations established by law, regardless of where such income was generated and regardless of the payer’s residence.”

So, as stated in the law, you have to declare in your personal income tax return your worldwide income earned during the tax year, in this case; 2025.

2. How to include the foreign work income in your Renta 2025

As we have checked before, it’s mandatory to include the worldwide income in your tax return, but there’s some options to be efficient with your Tax Return in Spain in 2025.

a. 7P LIRPF Exemption: Income received for work actually performed abroad

Article 7 of the LIRPF regulates all the tax exemptions from the income return point of view. Concretely, its article 7P states:

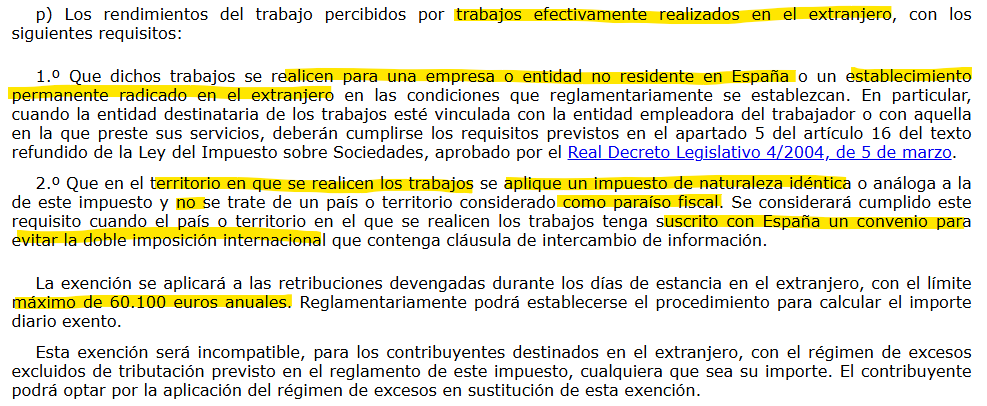

“p) Income from employment received for work actually performed abroad, subject to the following requirements:

1. That such work be performed for a company or entity not resident in Spain or for a permanent establishment located abroad, under the conditions established by regulation. In particular, when the entity for which the work is performed is related to the worker’s employer or to the entity where the worker provides services, the requirements set forth in Section 5 of Article 16 of the Consolidated Text of the Corporate Income Tax Law, approved by Royal Legislative Decree 4/2004 of March 5, must be met.

2. That in the territory where the work is performed, a tax of an identical or analogous nature to this tax is applied, and that the country or territory is not considered a tax haven. This requirement shall be deemed met when the country or territory where the work is performed has signed a double taxation avoidance agreement with Spain that contains an information exchange clause.

The exemption shall apply to remuneration accrued during the days spent abroad, up to a maximum limit of 60,100 euros per year. Regulations may establish the procedure for calculating the daily exempt amount.”

To sum up, the requirements to apply this exemption are:

The work should have been performed abroad

For a non residency company

That it exists an analogue tax to IRPF (income tax) in the country where the works are performed, or that the country has signed a DTA agreement with Spain

Limit of the exemption 60.100 € per year

b. Double taxation deduction (Foreign Tax Credit: the tax withholded in the country that paid the income)

This occurs when you earn foreign employment income that has been subject to a withholding tax (WHT) under the domestic laws of the taxpayer’s country of residence

Sometimes, domestic tax regulations require a withholding tax at source. Generally, this is provided for under non-resident tax laws, though the specific rules vary significantly from one jurisdiction to another.

When you have to include this employment income in your Spanish tax return, you can also deduct the WTH taxes paid abroad, HOWEVER…

🚩You cannot deduct the full amount if you have not checked the limits first!!!

The article 80 of the LIRPF regulates the procedure to calculate the amount that can be deducted from the FTC:

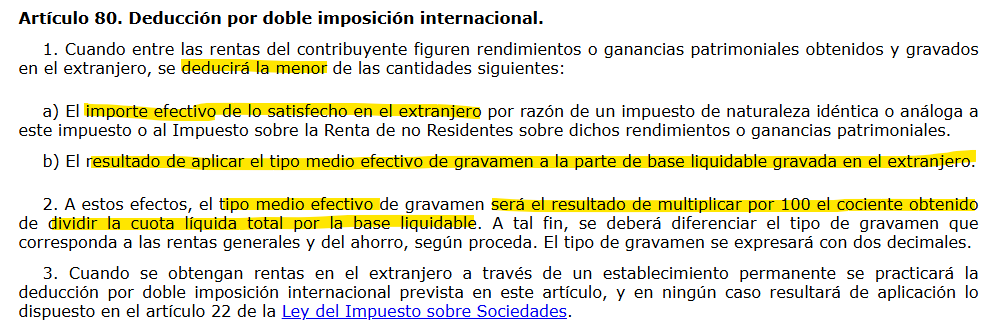

“Article 80. Deduction for International Double Taxation.

1. Where the taxpayer’s income includes income or capital gains earned and taxed abroad, the lesser of the following amounts shall be deducted:

a) The actual amount paid abroad by way of a tax of an identical or analogous nature to this tax or to the Non-Resident Income Tax on such income or capital gains.

b) The result of applying the average effective tax rate to the portion of the taxable base taxed abroad.

[…]”

The practical translation of the above is that you may not be able to deduct the whole withholded amount in the country of origin, while doing your Renta 2025.

You, or the person in charge of dealing with your Renta 2025, will need to calculate what is the maximum amount that can be deducted from the FTC.

3. What is the best option for my Renta 2025?????

Well, there is no absolutely right answer at 100% for each scenario to this question.

Considering that the Renta tax rate is progressive (meaning: the more you earn, the more you pay) , it’s correct to state that if you can decrease the amount of income, the final tax amount you will end up paying will also decrease.

Here’s an example:

Work income from the UK: 50.000€

Work income from Spain: 50.000 €

Withholding tax in the UK: 40% = 20.000€ (not real, just a suposition)

🅰️Option A: Exemption 7P LIRPF

Tax return 2025 in Spain:

Work income from the UK: 50.000€EXEMPTEDWork income from Spain: 50.000 €

Total income to include in Renta 2025: 50.000 €

TOTAL TAX BILL: 30% = 15.000 €

Total taxes paid: 35.000 €

In the UK: 20.000 €

In Spain: 15.000 €

As the work income from the UK is exempted, you cannot include the amount paid as withholding in the UK.

🅱️Option B: Double taxation deductions (FTC)

Tax return 2025 in Spain:

Work income from the UK: 50.000€

Work income from Spain: 50.000 €

Total income to include in Renta 2025= 100.000 €

Tax Rate for 100.000 € = 42% (not real tax rate calculation) = 42.000 €

Limit to the foreign tax credit: if the same base amount would have been received in Spain, meaning: how much 50.000€ are taxed in Spain?

Fictional Tax rate for 50.000 € is 30%, which are 15.000 €

Double international tax deduction (FTC accredit): - 15.000 €

Total tax bill:

Total income: 100.000 €

Tax rate 42%

Tax bill: 42.000 €

FTC: - 15.000 €

Total tax to pay = 27.000 €

Total taxes paid: 47.000€

In the UK: 20.000€

In Spain: 27.000 €

4. Conclusion

As you can see, the fact of excluding the foreign income that meets the criteria of Article 7P LIRPF, decreases the global tax rate of the taxable income.

The total amount in taxes paid between the source and the tax residency country, in general, is less if you use 7P than to accredit FTC.

Mastering the Spanish tax landscape is the ultimate act of professional empowerment for any expat. When you lead your fiscal strategy instead of fearing it, you unlock the true potential of your international career. Use the system to your advantage, understand your rights, and turn your tax residency into a strategic asset rather than a logistical hurdle